How does an industry growing toward $5.6 trillion still leave so many retailers struggling to explain last Tuesday’s underperformance?

The US retail market is heading toward $5.6 trillion in 2026, growing at 4.4 percent year over year, ahead of the ten-year pre-pandemic average of 3.6 percent. On the surface, those numbers look like an industry in solid health. Dig one level deeper and the picture changes. The US retail industry is not growing evenly. It is splitting, and the gap between the winners and the losers is widening at a pace that should demand the attention of every retail executive in North America.

This thought-leadership piece examines the structural forces reshaping US retail market trends in 2026, the data behind the bifurcated consumer economy, and what retail leaders need to do right now to position their businesses on the right side of this divide.

The US Retail Market in 2026: What the Numbers Actually Tell You

Total US retail sales reached $7.52 trillion in 2025, up 3.5 percent from 2024. In February 2026 alone, retail and food services sales hit $738.4 billion, a 3.7 percent year-over-year increase. Non-store retailers, a proxy for e-commerce and direct-to-consumer brands, grew 7.5 percent from the prior year. Food service and drinking places rose 5.2 percent. These are not struggling sectors.

But personal consumption expenditure growth is slowing. Moody’s Ratings projects real PCE growth of around 1.5 percent in 2026, down sharply from the 2.5 to 3 percent annual growth seen from 2023 to 2024. The consumer is still spending. The consumer is just spending more deliberately, more selectively, and more strategically than at any point in the past decade.

| 4.4% | Projected US retail market growth in 2026 – ahead of the 10-year pre-pandemic average of 3.6%. Total market size: $5.6 trillion. Source: National Retail Federation, 2026 Retail Outlook. |

The K-Shaped Consumer Economy: Understanding Retail Bifurcation in North America

PitchBook’s 2026 economic outlook describes a K-shaped economy in which the top portion of the consumer market splits upward while the middle falls away. In retail terms, this plays out in visit data, sales data, and margin data simultaneously. Placer.ai’s analysis of 2025 foot traffic found that off-price retailers and thrift stores gained significant ground. Luxury maintained modest growth. Mid-tier department stores continued to lose visits. Traditional middle-market anchors like Target and Kohl’s are contending with a genuine identity challenge in a market increasingly polarised between value and premium.

This is not a temporary cycle. McKinsey’s State of the US Consumer 2026 documents the paradox that defines the bifurcated retail environment: three in four consumers are actively trading down to cheaper brands, half are delaying discretionary purchases, and yet 65 percent remain willing to pay extra for two-hour delivery. Value and convenience coexist. What has disappeared is loyalty to mid-market brands that offer neither a compelling price point nor a compelling experience.

Four in ten Americans now show consistently deal-driven shopping habits, and seven in ten retail executives – surveyed independently by Deloitte say this is a permanent structural shift. Not a post-inflation hangover. A permanent restructuring of consumer behaviour in the United States retail market.

Private Label Growth: The $277 Billion Signal That Retail Leaders Cannot Ignore

Private label sales are projected to reach $277 billion by the end of 2025, surpassing the 2024 record of $271 billion. This is not a discount-aisle story. Walmart’s BetterGoods launch , its largest private brand food initiative in 20 years, represents a strategic repositioning to capture value-seeking consumers as a permanent customer segment, not as a cyclical accommodation. Private label growth in the North American retail market is outpacing the broader CPG industry.

At the same time, emerging brands are punching above their weight. Companies with less than 2 percent market share in their categories achieved 39 percent of category growth in 2024. The retail market in the US is simultaneously rewarding deep value and genuine differentiation. What it is not rewarding is the undifferentiated middle ground occupied by a significant share of legacy retailers.

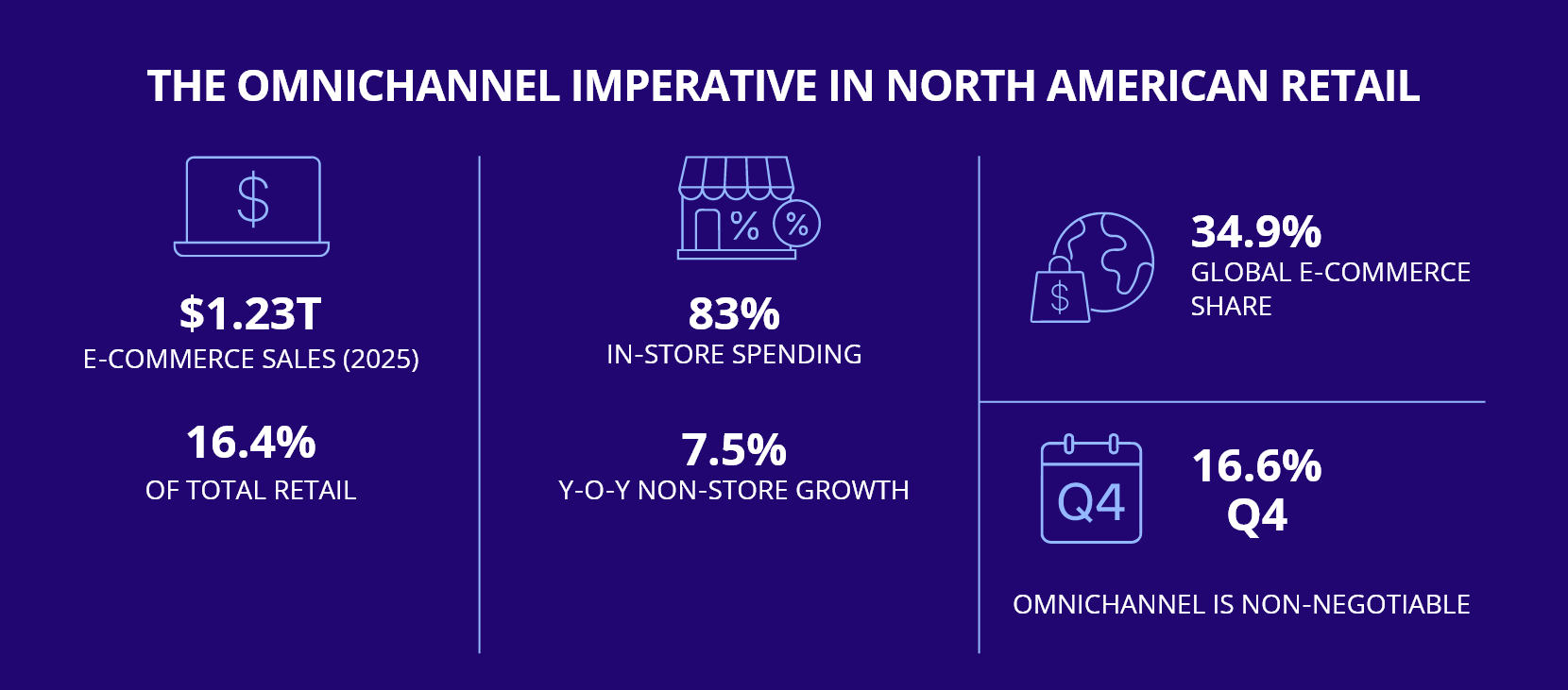

The Omnichannel Imperative in North American Retail

E-commerce hit $1.23 trillion in total US online sales in 2025, accounting for 16.4 percent of total retail sales, up from 16.1 percent in 2024. The fourth quarter of 2025 showed e-commerce at 16.6 percent of quarterly retail. Non-store retailers grew 7.5 percent year over year as of early 2026. North America accounted for 34.9 percent of the global e-commerce market in 2025.

These numbers matter for retail strategy in a specific way. Physical stores still account for over 83 percent of US retail spending. But the consumer journey increasingly begins online through search engines, AI platforms, and social commerce before it concludes in store or via delivery. Retailers who treat their channels as separate businesses rather than an integrated omnichannel operation are leaving both revenue and customer intelligence on the table.

Colliers’ Global Retail 2025 Trends and 2026 Outlook report identifies omnichannel integration as non-negotiable across North America. Retailers gaining ground in 2026 are those treating omnichannel not as a technology project but as an operations strategy – one requiring unified data across channels, store networks, and logistics infrastructure.

What Retail Market Bifurcation Means for Data Strategy

The retailers that performed through 2025 shared a common operational characteristic: they could see their business clearly enough to make fast, accurate commercial decisions. Trader Joe’s sustained momentum through a locally inspired assortment strategy and roughly 80 percent private-label mix. Off-price chains expanded by leveraging buying agility and inventory intelligence. Luxury players protected margin through tight supply discipline and customer data management.

None of that is achievable without a data infrastructure that matches the speed of the market. When 58 percent of shoppers are using generative AI tools instead of traditional search engines for product discovery, and when 67 percent report noticing AI-driven ads while browsing retailer sites and apps, the traditional analytics stack, built around weekly reporting cycles and backward-looking dashboards, cannot keep pace.

The business intelligence tools that won retail in 2019 will not win retail in 2026. The US retail market is moving faster, splitting harder, and rewarding precision over scale. Retailers who understand that and invest accordingly will build advantages that are genuinely durable. Those who treat data modernisation as a future project will find themselves rationalising losses against competitors who already made that investment.

Frequently Asked Questions: US Retail Market 2026

Q: What is the size of the US retail market in 2026?

A: US retail sales are projected to reach $5.6 trillion in 2026, growing at 4.4 percent year over year, according to the National Retail Federation. Total 2025 retail sales reached $7.52 trillion when including broader retail and food service categories.

Q: What are the biggest retail trends in North America in 2026?

A: The five dominant trends are: structural shift toward value-seeking consumer behaviour; accelerating AI adoption across retail operations; private label expansion to meet value demand; retail media network growth; and supply chain restructuring driven by trade policy uncertainty and tariff volatility.

Q: Why is the US retail market bifurcating in 2026?

A: The K-shaped economy is driving a permanent split between value and luxury retail. Middle-market retailers face pressure from both ends as consumers either trade down to private label and off-price options or maintain spending at premium and luxury price points. Mid-tier department stores are losing visits to both segments.

Q: How is e-commerce performing in the US retail market?

A: US e-commerce reached $1.23 trillion in 2025, a 5.4 percent year-over-year increase, accounting for 16.4 percent of total retail sales. Non-store retailers grew 7.5 percent year over year as of February 2026, outpacing the broader retail market.

The retailers that lead will be those that treat adaptability not as a defensive posture, but as a strategic capability. Focus on what is in your control, double down on the fundamentals, elevate them with AI and insight, and meet consumers with value. – Deloitte 2026 Retail Industry Global Outlook

How Infocepts Helps Retailers Navigate Market Bifurcation

Infocepts works with global retail enterprises to build the data infrastructure that turns market intelligence into commercial decisions. Through platforms like Decision360 and DiscoverYai, Infocepts delivers real-time analytics, demand forecasting, and personalised insight capabilities that give retail leaders the visibility to act precisely in a market that no longer rewards guesswork.

With over two decades of experience serving retail, CPG, and consumer industries, and a 97.2 percent client retention rate, Infocepts is the partner retail organisations choose when the stakes are high and the margin for error is low.

Ready to win in a retail market that’s splitting in two?

Leverage real-time data, AI, and unified insights to stay ahead of shifting consumer demand

Author

The Infocepts Retail COE brings together data and analytics specialists focused on helping retail and CPG organizations turn complex data into smarter decisions. From demand forecasting and inventory optimization to customer analytics and omnichannel performance, the team works at the intersection of data engineering, AI, and retail strategy.

Read Full Bio